Bangalore remains one of the most searched real estate markets among NRIs and for good reason. Strong rental demand, steady price appreciation, and an IT-driven economy make it a city that consistently delivers returns.

But buying property from abroad comes with its own set of rules. What you can purchase, how you transfer funds, what taxes you owe all of it is governed by a framework most NRIs have never had to navigate before. This guide walks you through every step

NRIs Buying Property in Bangalore: Is It Legal and What Are the Limits?

The short answer is yes. As an NRI, you are fully allowed to buy property in Bangalore under the Foreign Exchange Management Act (FEMA). The RBI has already granted generall permission no special approval needed before you purchase.

You can buy residential apartments, houses, and commercial properties. What you cannot touch is agricultural land, plantation property, or farmhouses anywhere in India, no exceptions. If a seller promises RBI approval for restricted land “later,” that is your cue to walk away.

NRIs Buying Propery Rules India 2026: What Matters Right Now

Under NRI property buying rules India 2026, the buying process has become more streamlined, but fund compliance is monitored far more closely than before.

According to the Reserve Bank of India’s FEMA guidelines (rbi.org.in), every rupee used for your purchase must come through legitimate banking channels. You can use funds from your NRE (Non-Resident External), FCNR (Foreign Currency Non-Resident), or NRO (Non-Resident Ordinary) accounts but never cash or informal transfers.

As per the Income Tax Department’s guidelines for FY 2025-26, TDS on property transactions involving NRI buyers is now tracked through Form 26QB with tighter scrutiny. Keeping a clean paper trail from day one protects you at every stage purchase, rental, and eventual sale.

Choosing Where to Buy in Bangalore

Bangalore’s residential market has seen sustained demand. According to the Knight Frank India 2024 report (knightfrank.com/research), Bangalore ranked among the top three Indian cities for residential property demand driven in part by NRI investment interest.

The right location depends on your goal.

If rental income is the priority, Electronic City, Whitefield, and Marathahalli have deep demand from IT professionals. Vacancy rates are low and rental yields are relatively stable.

If long-term appreciation is the goal, North Bangalore Yelahanka, Hebbal, and Devanahalli near the international airport has shown consistent price growth over the past three years. IVC Road in this belt is also seeing increasing developer interest, with infrastructure catching up fast. Read more on IVC Road Bangalore real estate insights if this corridor interests you.

If lifestyle and liveability matter most, South Bangalore neighbourhoods like JP Nagar, Bannerghatta Road, and Jayanagar offer established schools, hospitals, and social infrastructure ideal if you plan to eventually return and live there.

Ready-to-Move vs Under Construction: What Makes Sense for NRIs

This is a decision that carries more weight when you’re buying remotely.

A ready-to-move apartment gives you certainty. You see what you’re buying, there’s no construction risk, and rental income can start immediately after registration. The trade off is a higher price.

An under-construction project is priced lower at launch and typically appreciates by possession. But delays are common, and as an NRI you won’t be there to monitor progress. This makes the builder’s reputation critical. Before paying any booking amount, verify their past project deliveries, legal clearances, and RERA registration status.

For a full breakdown of how these two options compare on cost, risk, and return, read Ready to Move vs Under Construction Homes in Bangalore.

Documents You Need as an NRI Buyer

From your side: valid passport, visa or OCI/PIO card, PAN card, overseas address proof, and your NRE/NRO/FCNR bank account details. PAN is non-negotiable no property transaction in India can proceed without it.

From the seller or builder: sale deed, Encumbrance Certificate (confirming no legal dues), Khata certificate from BBMP, approved building plan, and the RERA registration number.

If you can’t be present in India for registration, a Power of Attorney (POA) allows a trusted family member or lawyer to sign and register on your behalf. The POA must be notarised and apostilled in your country of residence a step many NRIs overlook until it’s too late.

For a step-by-step verification checklist covering every document and approval you should confirm before signing, refer to Checklist Before Buying an Apartment in Bangalore 2026.

How to Transfer Money From Abroad

Transfer funds from your overseas bank to your NRE or FCNR account in India. From there, pay the builder or seller by cheque, demand draft, or bank transfer. Cash payments are prohibited and can jeopardise your ability to repatriate proceeds later.

The NRE account is fully repatriable when you sell the property, you can send the money back to your foreign account without any restrictions (up to two residential properties). This makes it the preferred route for most NRI buyers.

If you use an NRO account instead, repatriation is allowed but capped at USD 1 million per financial year. You’ll also need Form 15CA and Form 15CB, signed by a Chartered Accountant, to be submitted to your bank before the transfer.

Taxes NRIs Pay When Buying Property in Bangalore

Stamp Duty and Registration

Properties above ₹45 lakh attract 5% stamp duty plus 1% registration charges. Between ₹21 lakh and ₹45 lakh, it is 3%. NRIs pay the same rates as resident Indians no separate slab exists.

TDS When Buying

If the property crosses ₹50 lakh and the seller is a resident Indian, you deduct 1% TDS before payment and deposit it via Form 26QB on the Income Tax Portal. Most assume the seller handles this the deduction is actually the buyer’s job.

Capital Gains When You Sell

Hold for more than two years and Long Term Capital Gain tax applies at 12.5% as per Finance Act 2024. Sell earlier and your income tax slab rate kicks in. The buyer will deduct 20% TDS upfront at the time of sale you can claim a refund later when filing your Indian ITR, so plan your cashflow accordingly.

Getting a Home Loan in India as an NRI

Most major Indian banks SBI, HDFC, ICICI, Axis Bank offer home loans to NRIs, typically up to 80% of the property value. Interest rates generally range between 8.5% and 10.5% depending on the lender and your profile.

You’ll need foreign income proof: recent salary slips, employment letter, and six months of bank statements. If these are not in English, they may need notarised translation.

Repayments must come from your NRE or NRO account not from a foreign bank account directly. Setting up auto-debit from your NRE account keeps everything FEMA-compliant and avoids missed EMIs. For a complete walkthrough of the loan application process, read the Home Loan Process in Bangalore 2026 Guide.

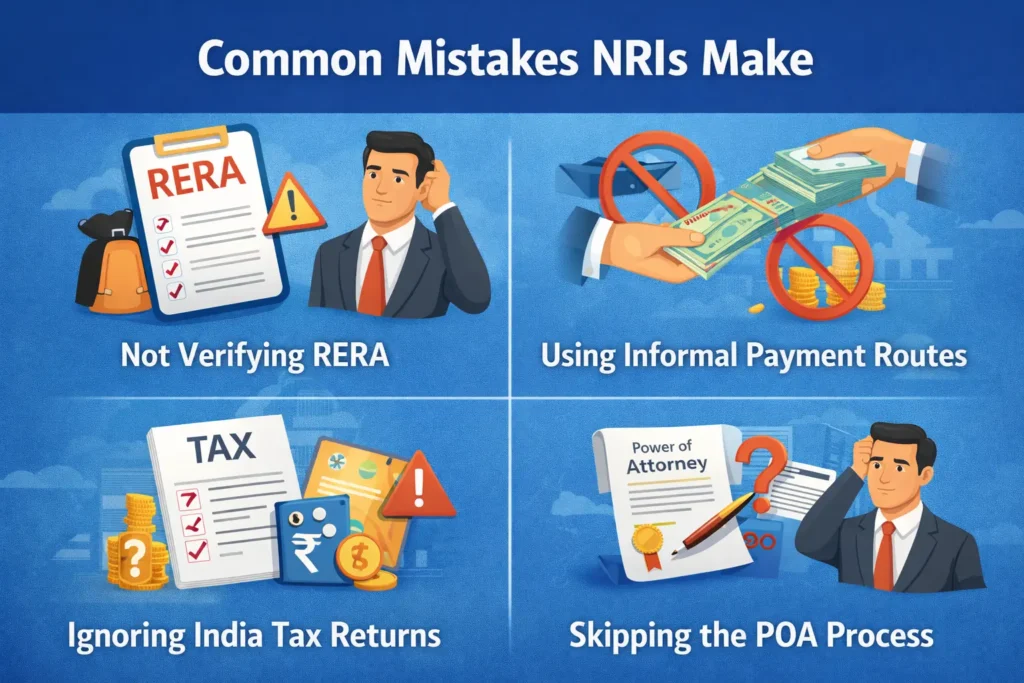

Common Mistakes NRIs Make

Not verifying RERA — Every project must be registered with RERA Karnataka before you pay even a token. Check at rera.karnataka.gov.in. Unregistered projects offer no legal protection.

Using informal payment routes — Any undocumented transfer creates a compliance gap that blocks repatriation and complicates your tax filing.

Ignoring India tax returns — If you earn rental income or make a capital gain from Indian property, you must file an ITR in India, even if the net tax is zero.

Skipping the POA process — An invalid POA can void your registration entirely. Get it properly notarised and apostilled before the deal moves forward.

Final Thoughts

NRIs buying property in Bangalore today have better tools, more regulatory protection, and clearer processes than ever before. RERA has changed the accountability landscape. Banking has simplified. The city’s fundamentals remain strong.

Go in informed, keep your money trail documented, choose a RERA-registered project, and work with a lawyer who understands NRI transactions. Bangalore has room for you make sure the property you buy there is worth coming back to.